This a long piece that would probably be better split up into several separate, focussed articles. Never mind, consider it as a rambling, idiosyncratic and opinionated mind-dump on the subject of the future of oil. I may later rewrite parts of it more coherently and rigorously for a wider readership. As I make my way through the recently published IEA WEO 2016, I will provide updates.

Pioneers or pariahs?

James Gandolfini, the late actor who played the gangster boss Tony Soprano, was once asked what profession he would never have wanted to have pursued. He answered: “an oilman” (video at 5:00). Those of us who have followed careers in the oil industry might be a little surprised, but not really that shocked, by a response like that. To many people, oil companies and the people who work in them are often seen as the embodiment of greed and environmental destruction. Oilmen get used to being thought of as pariahs.

It’s different seen from the inside. The work of oil exploration is well paid and intellectually challenging. When pushing the limits of knowledge in frontier settings, explorers have the privilege of interpreting new subsurface data for the first time. Unravelling the structure of the subsurface is a prerequisite for making the right investment decisions. Oil exploration is applied science at its best and those of us who have had a career in it can feel lucky indeed.

Over decades, the environmental performance of oil companies has improved dramatically, with much reduced footprints for exploration and production operations. This progress came not just as a result of tightening regulations, but also voluntary attempts to do a better job. Often, we found, measures that are more expensive at first turn out eventually to be cheaper as they become standardized. In addition, better practices build trust with communities and stakeholders. Importantly, employees take pride in work done well.

As an example, I was for a some years involved in seismic prospecting in the Canadian Rocky Mountain Foothills. Traditional methods of clearing seismic lines required bulldozing swaths of trees wide enough to drive trucks along. The straight cutlines were a visual blight and would take decades to grow back. We experimented with hand-cutting the undergrowth and delivering shot-hole drills and geophones by helicopter, keeping the forest canopy largely intact. Over a few years, the logistic techniques improved, the new style of shooting seismic data became cheaper than the old ways and the impacts became largely invisible. The regulators eventually caught up and made such techniques mandatory.

Everybody felt good about this. We were able to explore for essential commodities, natural gas and oil, with minimum local impact. Conservationists and recreational users had reduced reason to object and the oil companies earned the social licence to explore deeper into more rugged terrain and more sensitive areas.

However, there was one environmental impact whose importance emerged over the course of my career that could not be so easily fixed: climate change. Most people in the business, myself included, were reluctant to accept this. Many still can’t. It’s hard to acknowledge that the product that not only provides your living, but is also an indispensable commodity of modern society is inflicting irreversible damage to the habitability of the planet. When the culture of your workplace involves taking pride in extracting prosperity from deep in the Earth, it’s a really bitter pill to swallow to accept that the future of civilization depends on you no longer doing that.

People who work within the industry are often irritated by what they see as the hypocrisy of environmental activists who harshly condemn the producers while indulging in wealthy lifestyles that oil helps provide. They have a point. As someone who has made his living in oil and is now concerned about climate change, I too get accused of hypocrisy, although I suspect my critics really mean that I have been disloyal.

It’s not just personal biases that get in the way of accepting that the oil industry must soon die. The culture of the companies themselves and the societies they do business in leads to denial of their looming demise.

A small history of big oil

This section is informed by my own experience and by Professor Paul Stevens’ excellent Chatham House report: International Oil Companies: The Death of the Old Business Model .

The large privately-owned International Oil Companies (IOCs or”Big Oil”, for short) dominated the world’s oil supply up to the 1950s. The firms, known then as the Seven Sisters, formed an oligopoly that controlled not only the “upstream” side of the business (exploration and production), but also the “downstream” (refining and marketing).

As oil production increased after the Second World War, smaller private oil firms became a competitive force in global upstream markets, challenging the oligopoly of the IOCs. At the same time, most of the large oil-producing countries formed stated-owned firms—known as National Oil Companies or NOCs—that nationalized their domestic upstream industries. The formation of OPEC and the oil shocks of the 1970s demonstrated the market power of the NOCs. The global upstream dominance of the Seven Sisters was broken.

By the late 1970s nearly all of the major oil-producing countries in the developing world, the Middle East, Africa and Latin America, had at least partially nationalized their resource industries. This ruptured the vertical integration of upstream and downstream businesses that the IOCs had enjoyed and it enabled the formation of a global commodity market in petroleum. The oil price was now set by markets and the product itself became fungible.

The IOCs mostly retreated to exploration and development projects in the frontiers and in developed countries. Big finds were made in the North Sea, Alaska and elsewhere. However, oil-price slumps in the 1980s and after, combined with the increasing difficulty of finding large discoveries in areas without prohibitive operating costs, presented a challenge to the elephant-hunting ethos of the IOCs.

The IOCs retrenched, cutting costs and mostly getting rid of their research and development departments. While this focused attention on their core competency of managing risky projects and on the goal of enhancing shareholder value, it also marked an additional step towards the irrelevance of Big Oil. Service companies, like Schlumberger and Halliburton, picked up the slack and became the providers and developers of technology.

Prior to the 1980s, NOCs had to turn to the IOCs for technical assistance. Usually, this assistance came with demands for an equity share of the production. Once the IOCs had ceded their control over high technology to the service companies, the NOCs had the option simply to buy the best technology off the shelf.

All was not lost for the IOCs. They still had the skills and experience to provide project management for technologically difficult and hugely expensive projects. Risky business in inhospitable physical and political environments like the Arctic, ultra deep water, Sakhalin Island and Central Asia provided a niche that risk-averse and capital-limited nationalized companies could not easily fill. However, combinations of disappointing geology, disastrous execution and effective nationalization of projects by NOCs meant that these ventures were not always great investment success stories.

In the meantime, small private companies made many exploration successes in Asia, Africa and Latin America in new basins and in areas that had been prematurely deemed mature. Often, these discoveries would have been too small to have been material for the the big boys. But the finds added up and these successes showed developing countries that they no longer had to rely on the IOCs to raise risk capital and execute challenging exploration projects.

In the 2000s, upstart small and medium-sized companies operating in the US and Canada started to have great success with extracting natural gas and, later, oil, from “tight” (impermeable) reservoirs and shales. These discoveries eventually added up to enough production to depress N American natural gas prices after 2008. Later, fracking for oil helped cause the continuing global oil oversupply that halved the price of oil in 2014 and exposed the new powerlessness of the OPEC cartel. The oil business model evolved from conventional elephant hunting to one more like manufacturing, in which improved production technology and lowering operating costs became central to the new “unconventional” business model.

Even these events have not completely eclipsed the sense among the IOCs that their role in the world oil and gas markets remains an essential one. They still have huge fossil fuel and financial resources in absolute terms and they have mostly managed to replace their produced reserves by one means or another over recent decades. Moreover, there’s still a prevailing belief among many in the industry that oil is indispensable and that demand will rise forever. The IOCs increasingly pay lip service to the idea of unburnable carbon and stranded assets, but it’s not in their corporate DNA to fully accept this as a serious risk. If they did, that would mean acknowledging that they had no future as growing businesses.

By 2013, in relative terms, Big Oil was no longer living up to its name. In terms of production and reserves, the IOCs made up less than one-tenth of the global oil business. Before 1973, the Seven Sisters controlled 85% of the industry.

Stevens (2016) Chatham House report

The elaborate and glossily displayed scenarios that the IOCs develop for the future (see Shell’s Oceans and Mountains scenarios, for example) make the case that production will continue to grow for decades and that decline below today’s production levels will not occur until the latter half of the century, beyond the expected lifetimes of their investors and current management teams. Unsurprisingly, corporations find it hard to contemplate never producing their hard-won assets.

However, there are signs of change. Oil sands giant Suncor admits that leaving part of their resource base in the ground is essential for Canada meeting its emissions targets. The company acknowledges, as well, that it needs to reduce its emissions per barrel by 30% by 2030. Shell recently predicted peak global demand for oil in five to fifteen years, while still seeing its business continue for many decades to come. Exxon still envisages growing oil demand for decades, although low prices and high costs have forced the company to consider writing down its reserves by 4.6 billion barrels, 3.6 billion of which are in the oil sands.

Many companies have adopted internal carbon-pricing policies. Mostly, these are stress-testing exercises, designed to determine which projects are likely to be most vulnerable to future climate policies and carbon pricing. Some companies, like Shell, go further and actually apply an internal carbon price. This can provoke changes in operational behaviours that reduce upstream emissions. While such policies are laudable, they do not do the necessary job of real carbon pricing, which is to make all polluters pay for all of their emissions, including the end-users. It’s a bit like a tobacco company restricting smoking in their offices, while still selling cigarettes to the public.

The economist Anatole Kaletsky has argued (registration required) that it is now time for oil companies to kill themselves.

For Western oil companies,the rational strategy will be to stop oil exploration and seek profits by providing equipment, geological knowhow, and new technologies such as hydraulic fracturing (“fracking”) to oil-producing countries. But their ultimate goal should be to sell their existing oil reserves as quickly as possible and distribute the resulting tsunami of cash to their shareholders until all of their low-cost oilfields run dry.

That is precisely the strategy of self-liquidation that tobacco companies used, to the benefit of their shareholders. If oil managements refuse to put themselves out of business in the same way, activist shareholders or corporate raiders could do it for them. If a consortium of private-equity investors raised the $118 billion needed to buy BP at its current share price, it could immediately start to liquidate 10.5 billion barrels of proven reserves worth over $360 billion, even at today’s “depressed” price of $36 a barrel.

There are two reasons why this has not happened – yet. Oil company managements still believe, with quasi-religious fervor, in perpetually rising demand and prices. So they prefer to waste money seeking new reserves instead of maximizing shareholders’ cash payouts. And they contemptuously dismiss the only other plausible strategy: an investment shift from oil exploration to new energy technologies that will eventually replace fossil fuels.

It’s not just the oil companies that are struggling to face their own mortality. The oil producing nations and regions are also hooked, like most addicts, not just on producing oil, but on continually growing the business. Investors can quickly move capital to new businesses as old industries die, but, for countries and provinces that have come to depend on resource rents, it is much harder to adapt without economic suffering and cultural disruption. Capital is mobile, communities less so.

The curse of more

Source: Economist

The “oil curse” usually refers to the observation that countries rich in resources have worse development outcomes than those without. Countries with abundant oil or minerals tend to have more corruption, authoritarian governments, rent-seeking and inequality. Other industries do not develop because of high currencies and the resource industries sucking up all of the local talent. Economic development in resource-rich developing nations goes through wild cycles. In the long run, resource-deprived economies often grow more. Like tortoises and hares.

Rich countries with diversified economies and solid democratic institutions have avoided the worst of the oil-curse problems. Even resource-rich countries like Canada are not as dependent on oil and gas production as is commonly thought: its energy sector makes up less than ten percent of GDP. The notion that Canada is a petrostate like Venezuela or Kuwait is a gross exaggeration. Even so, the regions dependent on oil struggle to maintain economic stability. The cycles are just long enough to trick people into believing that they are permanent, that this time it will be different. As the familiar bumper sticker says:

Please God, give us another oil boom, we promise not to piss it away this time.

The boom phase of the cycle produces consumption, along with a sense of euphoria and entitlement among the population. Personal and government spending increases and there is political pressure to lower taxes. Thoughts of economic diversification become forgotten. Promises made to God during the previous bust get forgotten.

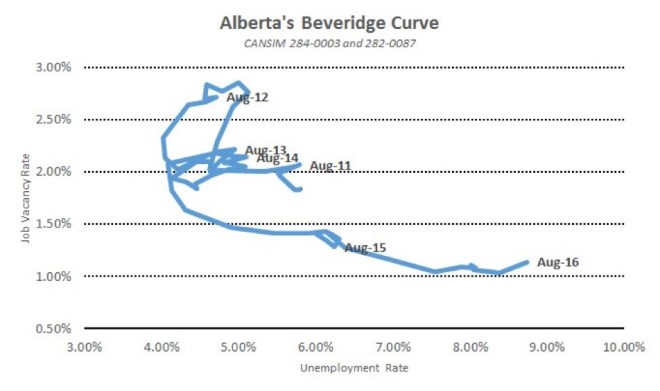

When the bust hits, as it did in 2014, brutal cost-cutting becomes a necessity for corporations struggling to stay solvent. New projects are shelved. Thousands of people are laid off and many families see their income reduced or eliminated altogether. For older folk nearing retirement, the pain is not too bad provided they have saved enough and invested in sectors outside the energy business. However, for young families with heavy mortgages, the suffering is acute and their dreams of a prosperous future die. The effects of the latest oil shock are continuing to worsen. As the figure below shows, job vacancies have halved and unemployment has doubled. Anecdotes from ex-colleagues suggest that unemployment among geologists and geophysicists in Calgary is now around 50%.

Via Trevor Tombe on Twitter

The provincial government faces a huge fiscal problem. A large chunk of government revenue comes directly and indirectly from oil and gas. When the price falls, royalty receipts diminish, along with revenues from personal and business income taxes. Alberta has lost more than $10 billion in annual resource payments over the past ten years or so, with gas royalties shrinking after gas prices collapsed in 2009 and oil royalties disappearing when oil prices fell in 2014. At the same time, demands grow on the government to provide for social services, healthcare and education. It is politically impossible for an Alberta government to even contemplate introducing a provincial sales tax (Alberta is the only province without one). The so-called “Alberta Advantage” of low taxation is an untouchable political third rail, even though a sales tax would provide a dependable and steady source of government revenue.

Raising royalty rates during a recession would only make the recession deeper. Drastic cuts in government spending would increase unemployment, worsen the economic downturn and increase suffering of the the most vulnerable. The only way that the government imagines it can balance its books is to hope for yet more growth in oil production. Maintaining production at current levels is, it seems, not an option, even though conventional plus oil sands production has just doubled in a decade. More is never enough.

When a politician says: “A lot of the oilsands oil may have to stay in the ground if we’re going to meet our climate change targets.” it is regarded as an insensitive gaffe rather than a statement of the obvious.

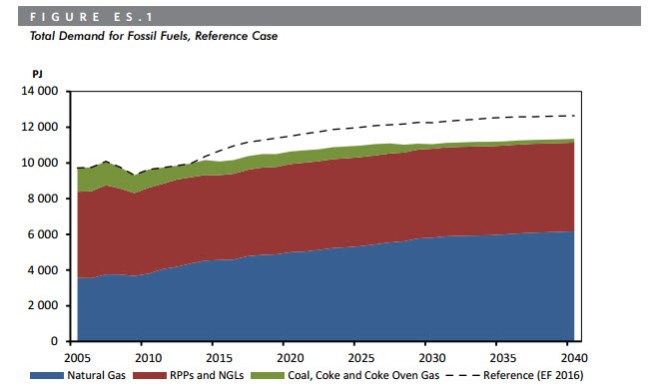

Source: CAPP

To its great credit, the centre-left government of Alberta has introduced a carbon tax in the midst of this bust cycle. An annual upstream emissions cap of 100 Mt of CO2 from oilsands operations has been instituted, which corresponds to 38% growth from today’s level of 72 Mt. If the carbon tax does its job, upstream emissions efficiency should increase, so a rise in production that stays within the emissions cap might be more like 50%, as shown in the forecast by the Canadian Association of Petroleum Producers, above.

It has become an article of faith in Alberta and in the government of Canada that continued oilsands growth is necessary. This growth, it is claimed, requires new pipeline infrastructure that will allow the development of new markets in Asia and elsewhere. The doubling of oilsands production in the past ten years has not been enough to produce economic stability or to balance the provincial books, but further growth of 50% by 2030 will allow Alberta to achieve lasting prosperity, or so the story goes.

Here are two graphs based on National Energy Board data, prepared by University of Calgary economist Trevor Tombe, from a recent Maclean’s article.

Eyeballing round numbers off these graphs and doing some arithmetic shows that with new pipelines, gross revenue from Alberta’s oil production should grow from about $50 billion annually in 2015 to about $150 billion in 2040 (I believe these are in 2015 Canadian dollars), roughly a tripling, or an annual growth rate of 4.7%. With no new pipelines, the gross revenues in 2040 would be around $125 billion; an increase of ~2.5 times over 25 years, representing annual growth of 3.7%. I don’t disagree with Tombe’s main point that blocking pipelines is an inefficient way to cut emissions compared to carbon pricing. But portraying, as many in Canada do, the provision of more pipelines as a national economic necessity is exaggerated. At sometime in the future, the reality of peak oil revenue will have to be dealt with.

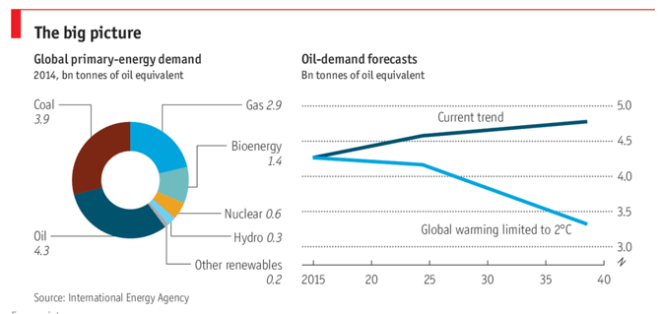

If climate change policies are effective, then global demand for oil will fall by 25% by 2040 according to the IEA. The following two charts come from a survey on the Future of Oil in The Economist. (The “Current trend” production is about 92 million barrels per day and the “2°C” value is about 64 mboe/day.)

Attempting a near-doubling of oil production in Alberta over the same period will pose challenges in securing growing market share in the face of shrinking demand. Moreover, Alberta bitumen is among the more expensive sources of oil and the world is awash with cheaper and cleaner reserves. Staking the province’s economic future on continuing growth in bitumen production is basically a bet that depends on the efforts to reduce global emissions failing.

[Note: The Economist made an error with the original version of this figure. The one above is the corrected version.]

The National Energy Board, as shown previously, foresees everlasting growth in oil sands production. The NEB fulfills the dual role of national energy statistician and the national energy regulator. The online newspaper the National Observer has revealed secret meetings between the NEB and politicians aimed at expediting the approval of pipelines. It hardly needs to be said that the NEB does not hold secret meetings with environmental groups to seek their advice on how best to prevent the pipelines being built. The NEB’s responsibility ought to be to even-handedly balance the interests of industry and the general public, but, in practice, it almost never turns a new development project down. As is the case with many regulatory bodies, it has been captured by the industry it is supposed to regulate and behaves more as a facilitator of industry expansion than a referee between competing national interest groups. The staff of the NEB are steeped in the assumptions of eternal growth of the the oil business, an industry in which many of them have been employed and in which some will hope to work again.

In its latest report Canada’s Energy Future 2016 update the NEB foresees national demand rising for fossil fuels from now until at least 2040, by about 10%. They admit that this growth will have to be revised downwards once they factor in national and provincial emissions policies, even though many of the provincial policies have been available for over a year.

As for oil production, the NEB sees it rising by 25% by 2040 even under their low price scenario, and by 70% under their high price assumption. These forecasts factor in declines due to depletion of conventional oil in Western Canada and the Newfoundland offshore, so the implication is that oilsands production will grow at greater than these rates. Declines in total oil production are thus deemed to be impossible even with their most pessimistic price projection. The forecasters say that: “Over the long term, all energy production will find markets and infrastructure will be built as needed.” The analysts are in the same organization as the regulator and there is an element of self-fulfilling prophecy in such forecasts.

Governments, regulators and oil companies are stuck with a group-think model of indefinite growth in demand. But demand for oil will likely fall even if climate policies fail. There are technological changes afoot that likely won’t be stopped.

Closer than they appear

Over 60% of the world’s oil is used for transportation and about half of that is used in passenger cars. Improvements in car engine efficiency are already making a big difference to oil consumption.

According to a recent report in The Economist:

The IEA says that such measures [US CAFE standards] cut oil consumption in 2015 by a whopping 2.3m b/d. This is particularly impressive because interest in fuel efficiency usually wanes when prices are low. If best practice were applied to all the world’s vehicles, the savings would be 4.3m b/d, roughly equivalent to the crude output of Canada. This helps explain why some forecasters think demand for petrol may peak within the next 10-15 years even if the world’s vehicle fleet keeps growing.

Two million barrels per day of excess production capacity was enough to cause a halving of the world oil price over the past two years. Relatively small changes in demand can lead to big changes in prices in the inelastic oil markets. Nobody can predict oil prices, but improving fuel efficiency in transportation will certainly exert powerful downward pressure.

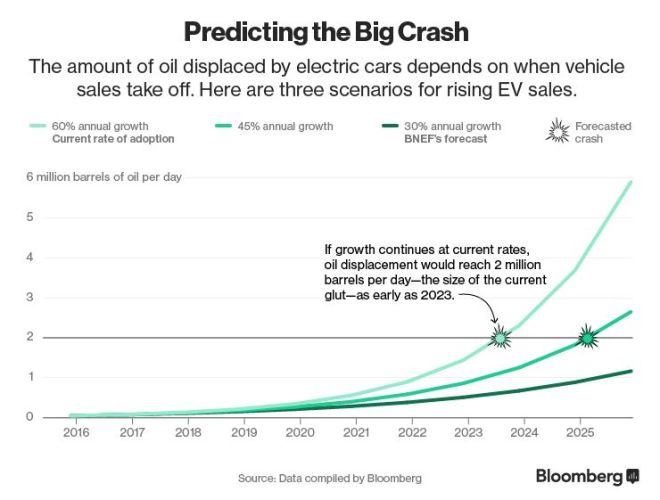

And then there are electric vehicles, which may reduce consumption even more dramatically. Falling battery costs and improved capacity are steadily moving EVs closer to economic parity with conventional gasoline engine cars. According to Bloomberg, this could happen in a decade or so. If EV adoption rates continue to grow at 60% annually, then 2 million barrels per day of oil consumption could be saved by 2023, growing to more than 15 million barrels by 2040. More modest growth rates, perhaps caused by rising electricity prices or stalled battery improvements, would delay these reductions.

There are some reasons to expect EVs to be adopted quickly.

- Although the technology is new, everyone who can drive a gasoline vehicle can drive an EV. The change will be easier than going from a film camera to a digital camera, or from a land line phone to a mobile.

- Roads and parking lot infrastructure is already in place. No new traffic laws will be needed.

- Several car manufacturers are investing billions in electrical drive trains.

- Some countries, like Norway are pushing EVs aggressively.

- Driverless cars and ride-sharing services like Uber will mean fewer vehicles driving more miles per year. This will improve the economics of EVs since extra capital costs will be written off sooner.

- For many suburbanites, EVs will work together well with rooftop solar to provide power supply/demand management.

- Vehicle range on a single charge will not be a problem for most users.

- Big European cities, like London and Paris have a serious problem with NOX and carbon particulate pollution from diesel vehicles. In London , for example, there are estimates of 9,500 premature deaths every year. That compares unfavourably with the estimated all-time 4,000 deaths from the Chernobyl disaster. Restricting access to city centres to electric cars, buses and delivery vehicles will solve this public health emergency.

- People gave up smoking not only because it causes cancer and costs money, but also because of more cosmetic reasons, like yellowing teeth and bad breath. Non-smoking quickly became cool and a status-marker. Similarly, electric cars already have an attraction to early adopters beyond saving money and reducing pollution.

To be sure, there are problems with providing charging infrastructure, but that’s just wiring. Also, there will be increased demand on the electric supply. According to Bloomberg, EVs could gobble up 10% of the world’s electricity.

India and China may take different paths than just making electric cars. As The Economist reports:

On the streets of big Chinese cities, the most eye-catching development is the surge in electric bikes, which cause far less congestion than cars and hardly any pollution, though their owners’ traffic etiquette is as poor as that of any car driver. (Delhi, not to be outdone, has acquired a new fleet of e-rickshaws). The IEA puts the number of electric bikes in China at 200m, nearly double the number of cars. They cater for workers who cannot afford cars, and overcome a problem that many public-transport users in big cities face: a long walk to and from the station.

The same article reports that India and China are also adopting different gas-powered vehicles (i.e., LPG, CNG and LNG). In my backyard, BC Ferries is about to introduce LNG-powered ferries.

Of course, nobody knows for sure how quickly EVs, economical gasoline engines and natural-gas-powered vehicles will eat Big Oil’s lunch. There will still be a need for oil for petrochemicals, as well as for marine and air transport. Oil is not going to go away altogether, but the industry paradigm of eternally increasing demand appears doomed. Peak oil demand is closer than it may appear.

The looming irrelevance of big oil companies

Some big oil companies are attempting to avoid obsolescence by getting into new lines of the energy business, for example, renewable energy and biofuels. This is probably doomed to failure because there is no reason to expect these corporations to have any comparative advantage over specialized start-ups. In the past, many oil companies have tried to rebrand themselves as energy companies rather than what they really are: providers of liquid and gaseous hydrocarbon fuels. BP famously tried this and failed by rebranding the company Beyond Petroleum. Other oil companies have unsuccessfully attempted to diversify into geothermal energy, coal and even nuclear energy.

If oil company shareholders have any sense, they will demand that the companies stick to their knitting and, as I quoted Anatole Kaletsky writing earlier, demand that they blow down their assets, paying fat dividends to shareholders who could then reinvest their returns elsewhere. The development of digital cameras did not depend on Kodak: the development of clean energy will not require the participation of Big Oil.

There are two areas in which oil companies could have better success in leveraging their expertise. One is to refocus on natural gas. According to the IEA World Energy Outlook 2016, peak gas demand is as equally imminent as oil in their 450 scenario, but is more likely to plateau than plunge.

The problem with gas is that there’s even more of it than there is of oil. Thanks to fracking, N America has a glut of gas and prices are so low that the industry is struggling to get by. There’s an oversupply of LNG in the world and new projects, from BC for example, are uneconomic at current prices. Russia, Central Asia and the Middle East have more gas than they know what to with. Sooner or later, somebody is going to figure out how to transfer the N American fracking boom to other continents. Gas is not likely to have fat profit margins at any time in the near future and the growth prospects for the IOCs as natural gas companies are probably limited.

The other area where the IOCs have real expertise and growth potential is in carbon capture and storage. Most of the mitigation scenarios for keeping global warming below two degrees employ huge amounts of CCS. I have previously written skeptically about our ability to deploy CCS, at scale and in sufficient time, at Corporate Knights Magazine , in the Bulletin of the Atomic Scientists and on this blog.

Despite my skepticism, some application of CCS is probably going to be essential in limiting emissions. There’s little doubt that the big oil companies are technically and organizationally the best equipped corporations to undertake the massive work of CO2 sequestration. Having made a successful business out of extracting carbon from geological reservoirs, it would not be difficult for IOCs to retool to reverse the process. The problem is that, in the absence of government grants or serious carbon pricing—more than $50/tonne CO2e—there is no business case to do it.

Climate campaigners are often obsessed with confronting the big oil companies. It is certainly true that many of these companies once played an active role in sowing doubt about climate science and that to this day some corporations subvert climate policy, particularly in the USA through political donations and lobbying. This past and present behaviour is deplorable. Although pressuring the big companies with lawsuits and shareholders resolutions may be cathartic, ultimately it will not, I think, get us very far. Big Oil never had the ability to solve the climate crisis and their power to slow progress is now greatly reduced, because the drivers of mitigation are now being unstoppably driven by technology and, after Paris, an international political consensus on action. The Economist argues that even the election of Donald Trump will not be enough to stop international climate action.

Too much activist focus on oil companies is not just a distraction, but may even be counterproductive, since it bolsters the myth of Big Oil’s indispensability. Increasingly, the IOCs are facing irrelevance. They are not going to disappear altogether, but they will soon lose their place at the commanding heights of the industrial hierarchy.

Late edit: this is the conclusion to Paul Stevens’ excellent Chatham House report International Oil Companies: The Death of the Old Business Model which sums up the overall argument nicely.

The IOCs face major challenges. Since the early 1990s, a number of problems undermined their old business model. This has been aggravated by two more recent problems: issues associated with ‘unburnable carbon’ and the collapse in crude oil prices seen since June 2014. While the IOCs have been able to survive the last 25 years, more recently real cracks have begun to show. The symptoms are poor financial performances and growing disillusion on the part of their shareholders with a business model rooted in assumptions of ever-growing oil demand, oil scarcity and the need to increase bookable reserves. These assumptions increasingly lack validity. There are possible solutions for the IOCs. However, none alone is sufficient, and even together they would amount to fiddling around the edges while the model continues to undermine the companies’ prospects for survival. In particular, the IOCs cannot assume that, as in the past, all they need to survive is to wait for crude prices to resume an upward direction. The oil markets are going through fundamental structural changes driven by a technological revolution and geopolitical shifts. The old cycle of lower prices followed by higher prices can no longer be assumed to be applicable.

In this new world, the only realistic option for the IOCs lies in restructuring and realizing many of their current assets to provide cash for their shareholders. This means inevitably, however, that they must shrink into the remaining areas, functionally and geographically, where they can earn an acceptable return. This requires a major change in the corporate culture of the IOCs. It remains to be seen whether their senior management can manage such a fundamental shift. If they can, then the IOCs will be able to slip into a gentle decline but ultimately survive, albeit on a much smaller scale. If they do not change their business model, what remains of their existence will be nasty, brutish and short.

{kind=link}

Pingback: The looming irrelevance of big oil – Enjeux énergies et environnement

Minor typo:

“If climate change policies are effective, then global demand for oil will fall by 25% by 2014 according to the IEA.”

Do you mean 2040?

Thanks, Blair. Yes, corrected.

Good article by the way

Great article, Andy, thanks for setting things straight.

Kind of a tangential issue, but I found the part about Canada not being a petrostate interesting because the loonie is so responsive to the price of oil. Could it be that Canada’s costs are so high that small fluctuations in the oil price are much more significant to its national income (GDP, whatever) than those same fluctuations would be to a gulf state, where costs are only in the single digits per barrel?

It’s true that the Canadian dollar does fluctuate in sync with oil prices. I’m guessing that this is because oil, although a small percentage of GDP, makes up a larger proportion of Canada’s exports. Hence, the currency gets sideswiped. That’s off the top of my head and I don’t have the stats to back that up at hand.

The fluctuating C$ actually helps the oil industry a bit, because the oil price in local currency is smoothed out a little compared to quoted prices in USD.

Two queries:

1. would this scenario of winding down exploration and paying out fat dividends also make much higher royalties possible?

2. do the oil companies actually own the oil or do they own the rights to develop it? If they are not going to develop it, might some fraction of these reserves revert to the political jurisdictions in which they are found?

1) If governments make royalties too high in times of low prices, then the companies may decide to shut-in production. If prices are high enough to allow for fat dividends, it’s quite possible that governments might well decide they want a bigger share of the rents. Governments usually want companies to reinvest in exploration and development and they might be ticked off with companies simply blowing down their assets. It’s conceivable that governments might try to institute a royalty, tax and incentive regime to induce more reinvestment. But, really, I’ve no idea how things might play out should companies decide not to reinvest for fundamental strategic and economic reasons, and I’m just thinking aloud. Fiscal and licensing regimes assume that companies will want to grow their assets, not liquidate them.

2) Yes, in most non-OPEC countries the oilcos have contractual production-sharing agreements that grant title of the resources or a share of the resources to the company. This means that the company can book reserves as assets that show up on their balance sheets and sell the rights to third parties if they wish to. (In some countries with nationalized resources, such contracts may not be allowed by their laws. In such cases, contracts with foreign companies may compensate the contractor with cash for its exploration and development efforts, while keeping the oil as 100% belonging to the government. Such arrangements are not popular with western oilcos, because they usually want to be able to book reserves.) In any case, to answer your question, if oilcos decide not to develop resources, they typically would revert to the original rights holder, usually a government, but it could also be a freeholder or, say, an aboriginal title holder.

I will so deeply enjoy watching Saudi Arabia wither up and die.

The Saudi Arabia regime is repellent in so many ways, that I’ll join you in welcoming its demise. But when it goes, the majority of the Saudi people are going to suffer horribly, while the ruling classes will scuttle off to safe havens. It won’t be fun to watch.

Andy,

Oddly I was just thinking of you as I was writing this. I’m doing a ton of guesswork, nowhere near as informed as you, and I come to a different conclusion: Big Oil is trying to NOT become irrelevant, which is why Exxon is signalling to Trump that they don’t want him to pull out of Paris.

I will read your excellent post here in more detail than I already have, in the meantime I’d appreciate it if you could let me know if my outsider’s instincts are more or less going in a direction which somewhat resembles the truth. Thanks!

I don’t think there is any contradiction, in what we are arguing. You are saying that oilcos are trying to avoid irrelevance. I’m arguing that irrelevance will be thrust upon them.

Of course, my pessimism may be misplaced and some oilcos may be able to reinvent themselves as new energy companies. But I see it as more likely that the financial and human capital in today’s oilcos is highly mobile and is more likely to find a successful home under a different corporate structure and culture, one better equipped to develop an alternative energy business.

Thanks, Andy.