A bungled correction to a Globe and Mail article reveals that the intent was to publish a puff piece on the oil sands, not an objective analysis of the future of bitumen production in the face of serious climate change mitigation.

Just over two weeks ago, I wrote a piece critical of an article in the Globe and Mail: Environmentalists should end the charade over the oil sands, written by Martha Hall Findlay and Trevor McLeod. I also contacted the editor at the G&M to alert him/her of the errors in the piece. I revisited the G&M article recently and found the following note at the bottom.

Eds Note: This version clarifies references to the IEA’s outlook for oil to 2040.

I didn’t keep a copy of the entire original article, so I can’t be sure of all the updates they made, but I did cite the problematic first paragraph of the original piece (the words that were later removed are marked with a strikethrough):

The story starts with global energy forecasts. Even if there is very aggressive adoption of electric vehicles and renewable energy technologies – which we wholeheartedly support – the world will use more oil each year through at least 2040. According to the International Energy Agency (IEA), if the world goes beyond the aggressive commitments made in Paris and achieves the 2C global goal, then oil demand would fall

by2040. Yet, oil demand will remain high for years afterthat.

The “clarified” version follows, with text underlined

The story starts with global energy forecasts. Even if there is very aggressive adoption of electric vehicles and renewable energy technologies – which we wholeheartedly support – most forecasts, including two of the three International Energy Agency (IEA)’s scenarios, predict that the world will use more oil each year through at least 2040. According to the IEA’s third forecast, even if the world goes beyond the aggressive commitments made in Paris and achieves the 2C global goal, which many analysts doubt, then oil demand would fall before 2040. Yet, even in that most aggressive scenario, oil demand will still remain high for years after 2040.

I suppose it’s fairly standard for newspapers to try to save face by claiming to “clarify” rather than “correct” a piece. However, in this case they also introduced new errors and added confusion.

Incidentally, they didn’t acknowledge me having pointed out the errors in the article, either publicly or privately. Perhaps others got there first.

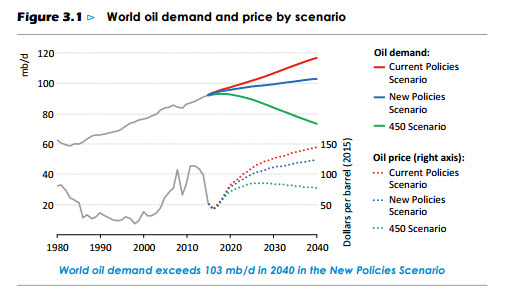

Here are the IEA scenarios again:

The first correction: “most forecasts, including two of the three International Energy Agency (IEA)’s scenarios, predict that the world will use more oil each year through at least 2040.” is correct as far as the three IEA scenarios go. But it is a little misleading to claim that “most forecasts” predict rising demand beyond 2040. It is true that some oil companies are confident of oil demand increasing for many decades, but expert opinion is split and the fact is, nobody really knows. It would make sense for everybody with a stake in oil’s future to acknowledge that there is huge uncertainty. Investors in new infrastructure should at least recognize that falling oil demand is a possibility over the next decade or two.

For example, Shell, quoted in Bloomberg:

Royal Dutch Shell Plc, the world’s second-biggest energy company by market value, thinks demand for oil could peak in as little as five years, a rare statement in an industry that commonly forecasts decades of growth.

“We’ve long been of the opinion that demand will peak before supply,” Chief Financial Officer Simon Henry said on a conference call on Tuesday. “And that peak may be somewhere between 5 and 15 years hence, and it will be driven by efficiency and substitution, more than offsetting the new demand for transport.”

The World Energy Council has a range of musically-themed scenarios, two of which foresee peak oil demand in 2030:

Oil peaks in 2030 in Modern Jazz at 103 mb/d and at 94 mb/d in Unfinished Symphony. Despite growing demand for transport fuels, new technologies and competition from alternatives drive diversification and lead demand to slow beyond 2030. Hard Rock sees status quo transport systems dominate. As a result, oil sees a peak and plateau of about 104 mb/d between 2040 and 2050. Unconventional oil reaches 15-16mb/d in Modern Jazz and Hard Rock. MENA remains the dominant oil producer to 2060 in all three scenarios.

McKinsey sees a demand for liquid hydrocarbons rising because of a growing petrochemical industry, whereas demand for oil for transportation peaks in 2025.

The total demand for liquid hydrocarbons will play out as a tug of war between growth in the petrochemical sector and declining demand from passenger cars. Petrochemical feedstock will drive 70 percent of the growth in demand for liquid hydrocarbons through 2035. Demand for liquids, excluding chemicals, will peak and flatten by 2025 because of a decline in demand from light vehicles. The petrochemicals demand will drive the growth of light end products, a large share of which are not made from crude oil.

Note that the robust liquid hydrocarbon petrochemical demand favours light-end products such as condensate and natural gas liquids. These are produced as as by-products from natural gas production such as the Montney play in BC and Alberta. Ultra-heavy crudes, such as bitumen would not be preferred feedstocks for petrochemicals.

Predictions of peak oil demand before 2040 are not all from starry-eyed environmentalists enraptured by EVs and solar panels. Serious, well informed players in the oil business are starting to consider looming peak oil demand as a serious risk.

A second “clarification”: “Yet, even in that most aggressive scenario [IEA’s 450], oil demand will still remain high for years after 2040.” The writers avoid saying that in this scenario, demand actually peaks in 2020.

The IEA doesn’t actually predict the oil demand after 2040, but simple extrapolation would show demand falling at roughly the same rate that demand rose from 1980 to 2010. By 2040, global demand will be back to late 20th Century levels. This is not exactly demand that will “remain high”. The rate of demand decline, about 1.5% per year, is slower than the typical rate of depletion of a typical oil well, so some capital will be needed to stop production levels falling faster. Nevertheless, the annual decline in demand will be enough, ceteris paribus, to put significant downward pressure on prices. This will discourage expensive, long-term oil exploration and development. Falling demand will transform the global oil industry.

Finally, the notion that “many analysts doubt” that we will achieve the Paris goals is unfortunately all too true. Countries have, for decades, talked the talk about cutting emissions while promoting their domestic fossil fuel production businesses. In fact, it is exactly the kind of message put forward by Hall Findlay and McLeod—tackling climate change is compatible with expanding fossil fuel production and consumption—that has led us into this situation where maintaining a stable climate has now become very difficult.

The “many analysts doubt” phrase was missing from the original article, which wrongly claimed that oil demand growth would occur even as we met the Paris targets. Now that they have realized their error with picking the wrong IEA scenario, the writers have suddenly decided to highlight the widespread doubt in achieving the sub-2°C goal. They maintain their narrative that oil demand will rise for decades. This is revealing. Clearly, the main point of their piece was to make a case for continued oil sands production. Their argument that rising oil demand is compatible with meeting the Paris targets was incidental and conveniently abandoned. In other words, it was a puff piece for the bitumen business, not the objective examination of bitumen extraction and climate targets that it pretended to be.

Why most bitumen will stay buried

It’s unlikely to be made-in-Canada emissions-control measures that doom the oil sands despite the rhetoric from the right in Alberta. With a carbon tax and an emissions cap in place, companies will be have incentives to reduce emissions and there’s little doubt that progress will be made. Lower emissions will quite possibly mean lower costs, since less energy will be wasted in the extraction process. It’s possible that emission pricing and caps may even help the viability of the bitumen business in the long run.

The critical factor determining the fate of the growth of oil sands production will be economics, especially in a world of shrinking demand. Low prices will certainly put downward pressure on production costs and this will help bottom lines. The same pressures will act on the competition, too, so improvement relative to other oil production areas may not happen, even as absolute costs go down.

The oil business has changed. No longer is it a business characterized by big-game hunting on the wild frontiers and lavish mega-projects in hostile environments. Increasingly, it is an industry in which the winners will be those who can cut their costs to the bone and keep cutting them. It used to be that the oil exploration business was a little like trying to make a Hollywood blockbuster. You needed imagination, technology, capital and luck. More often than not you produced a dud, but the big successes paid for the failures. It was a lot of fun while it lasted. Now, the future of the industry looks a lot more like a manufacturing business, in which reducing costs and increasing efficiency are everything.

New oil sands projects require huge capital outlays (billions) up front and long lead times from the project sanction to first oil. In contrast, US tight oil development needs smaller chunks of capital investment (millions) and new production can be achieved in months rather than bitumen’s years. In a world in which new technologies and the prospect of tightening emissions regulations threaten the omnipotence of oil as a transportation fuel, nobody can be assured of rising or even stable demand and accompanying escalating prices. Add to this the fact that bitumen carries a hefty price discount relative to light crude oil because of its chemistry—it has too little hydrogen and too much sulphur. Compared to lighter blends, bitumen is not the best feedstock for making gasoline and it is not in demand for making petrochemicals.

We may have already seen the last of the big greenfield oil-sands developments. Canadian politicians will no longer be able to rely on Alberta being the sweet spot of the national economy. To be sure, production of bitumen will persist for decades, but profits are likely to be modest and growth will be slow or stalled. Articles like Hall Findlay and McLeod’s may be reassuring to people hoping for a future in which oil sands production prospers while we reduce emissions. Many commentators in Canada and in Alberta, in particular, refuse to imagine a future without a thriving oil business. But perhaps it’s time to look beyond yesterday’s economic boom industry and instead focus on the new businesses that will power the future.

It doesn’t surprise me that Hall Findlay and McLeod either hadn’t done their research or were prepared to actively mislead the public – after all, their job is to promote the industry come what may, with “alternative facts” when necessary. What is more disturbing is the failure of the Globe and Mail to address this disinformation campaign honestly.

First and foremost, I have no disagreement with your analysis of the economics and long-term future of capital-intensive fossil fuel projects, in particular heavy oil and bitumen. One thing I would like to see more of are studies of how the price and availability of condensates would affect bitumen production and shipping… I think this issue has been skated over by many analysts.

As for that Globe and Mail comment piece, it’s typical of newspapers to admit to errors only grudgingly, to the least extent possible, and never to credit those who pointed them out.

In the case of op-ed contributions, solicited or not, the perceived responsibility for the accuracy of content is even lower. (“It’s just an opinion. If you disagree, feel free to submit your own.” Which, of course, is rarely published. “We just ran something on that.”)

It doesn’t surprise me that the senior management of some large oil and gas companies have a clearer view of matters than their cheerleaders in the media. Despite the obvious psychological incentives to look on the bright side, such companies are led by reality-based, practical individuals. (I leave aside any questions as to their ethics and long-term judgement.)

Harder to explain are the consistently and by now obviously wrong forecasts by agencies such as the International Energy Agency and the U.S. Energy Information Administration. (IEA and EIA – no chance of confusion there!) Are such agencies co-opted by the short-term economic interests of their funding governments? Are they just ultra-conservative and fear looking ‘unserious’? Or do they lack skin in the game and are thereby insulated from the costs of being wrong?

I think that you got it exactly right with your comment on having skin in the game.

It has become impossible for “serious” commentators in Canada to contemplate a future without the oil sands. It is perhaps not surprising that people in Alberta, already facing relative economic hardship, don’t want to acknowledge the prospect that there may never again be a big investment boom and its accompanying royalties. Every political party in Alberta is betting on expansion and commodity price increases.

But it goes beyond that. Justin Trudeau’s Liberals also are rooting for a rebound and find themselves unable to say anything that could be construed as pessimistic about the future health of bitumen extraction. They maintain this stance despite saying they are committed to the Paris 1.5-2°C climate targets. Then there are the various think tanks and captured regulatory agencies who see their job as industry cheerleaders rather than objective analysts.

It can look different when you are responsible for allocating capital, either within the oil industry or within the economy as a whole. To be sure, some oil men are more optimistic than others about the oil sands. However, it will be very interesting to see if the KeystoneXL project can retain industry support. If it does not, that would be a big psychological blow to the oil sands optimists.

Amory Lovins has a piece just out about KXL and what he sees as the imminent demise of the oil sands. I think he’s too gung-ho about EVs (I would like to be wrong about that) and he’s mistaken to imply that prices of $70/bbl are needed to sustain production. Those kinds of prices are required to build new projects, but already operating projects with sunk costs can probably maintain production at current prices. There are other minor problems with his article, as well, but you can’t deny the guy’s ability to make a strong, if overstated, case.

https://www.forbes.com/sites/amorylovins/2017/03/26/keystone-xl-pipeline-gusher-of-financial-risk/#48e71d2dde68

With respect to large-scale new, expanded, or refurbished pipelines, I suspect much will hinge on contractual details.

If pipeline operators expect producers to shoulder too much of the long-term financial risk (or vice-versa), I could see such projects getting jammed in multi-billion dollar games of chicken.

Not sure what the Trudeau government’s strategy is. Is it trying to say vaguely reassuring things to the O&G industry while quietly hoping projects will be cancelled due to external economic forces? I suppose one way to tell would be if it enacted clearly favorable laws and regulations for the industry, or provided direct or indirect financial assistance per aerospace and automotive sector precedents. The latter seems very unlikely, frankly, but you can never be certain.